Robo-Advisors have become extremely popular in the last few years with companies like Wealthfront and Betterment making up most of the market share. These companies essentially create and manage a portfolio of low cost index funds for a .25% annual fee. This is a much cheaper option than giving your money to a hedge fund manager, but also more expensive than simply doing it yourself with a simple portfolio of index funds. So which one is right for you, Robo-Advisors or DIY Index Fund Investing?

What Are Robo-Advisors?

Compared to traditional money manager or hedge funds that charge 1% (or more) a year to, to “manage” your investments, Robo-advisors are a much cheaper alternative. You will be able to get a diversified portfolio that is automatically rebalanced and offers tax loss harvesting for about a quarter of a percent.

One of the best parts about robo-advisors is that you basically just set it and forget it. You can pick an amount that you want to invest on a monthly basis and then the robo-advisor does the rest. Automatically buying your new index funds and rebalancing ones that have either over or underperformed.

For someone who wants a completely hands-off approach, choosing a Robo-advisor is one of the easiest ways to automate your investing and build long term wealth.

Get Your First $5,000 Managed for Free with Wealthfront

Build Your Own Index Fund Portfolios

I started out by investing in low cost ETFs with Charles Schwab. I wanted to learn more about investing and thought that I could manage it myself and I also had fun doing in (while the market was going up). I quickly realized that I wasn’t able to look at my investments objectively and trying to rebalance them myself every month became a chore.

I became my own worst enemy and tried to “time” the market. This worked out sometimes and I was able to sell before a correction but would then miss the buying opportunity. More often than not, I would have been better off leaving the entire amount in and forgetting about it. Every experienced investor will tell you that you can’t time the market, but every novice investor still wants to try.

Every experienced investor will tell you that you can’t time the market, but every novice investor still wants to try.

Around this time I started hearing more and more about Robo-Advisors and decided to give Wealthfront a try. The best thing about it was that it was completely automated. A certain amount was deducted from my checking account every month and I never had to even think about it. It was also in a separate account from my checking account so I barely ever looked at the short term fluctuations.

But I couldn’t help but think about the 0.25% yearly fee that I was paying. It sounds like a small amount but this is charged every year and I plan on keeping the majority of my money invested. As my investment grew, the amount I was paying really started to add up.

Robo-Advisor Fees:

$10,000.00 = $25.00 Yearly Fee

$50,000.00 = $125.00 Yearly Fee

$500,000.00 = $1,250.00 Yearly Fee

$1,000,000.00 = $2,500.00 Yearly Fee

I decided to find another automated way of investing. I didn’t want to sit down every month and buy ETFs but I also didn’t want to pay for something I could easily do myself. That lead me to Automatic Mutual Fund Investing with Charles Schwab.

Automatic Index Fund Investing

Building an Automated Portfolio using low cost index funds is the best of both worlds. It’s completely hands off and has lower cost than Robo-Advisors.

The funds are automatically withdrawn from my checking account and invested into a portfolio of low cost index funds. I no longer need to pay the 0.25% fee for a robo-advisor and I don’t need to manually buy ETFs like I was doing in the past. My investment strategy is now completely automated and has the lowest possible cost.

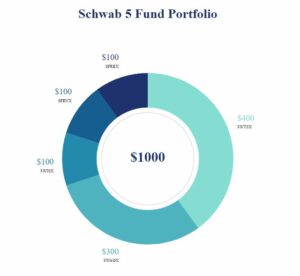

I used Schwab to Build an Automatic 5 Fund Portfolio:

40% – SWTSX – Schwab Total Stock Market Index Fund – Net Expense Ratio 0.030%

30% – SWAGX – Schwab Us Aggregate Bond Index Fund – Net Expense Ratio 0.040%

*Bond Funds Can be Subsituted with Schwabs Money Market Fund SWVXX*

10% – SWISX – Schwab Big International Companies Index Fund – Net Expense Ratio 0.06%

10% – SFREX – Schwab Fundamental Global Real Estate Index Fund – Net Expense Ratio 0.390%

10% – SFENX – Schwab Fundamental Emerging Market Large Companies Index – Net Expense Ratio 0.390%

Learn How to Build Your Own Index Fund Portfoilo Here!

FAQ

Q: Do Robo-Advisors Use Index Funds?

A: Robo-Advisors usually use low cost ETFs or Mutual Funds which track popular index funds. However, they also charge a fee on-top of the fee charged by the index funds.

Q: Are Robo-Advisors Better Than Mutual Funds?

A: Paying a mutual fund advisor is usually not a recommended strategy because in most cases you’re paying this advisor about 1% to manage your money. Robo-Advisors are cheaper than this and building your own fund using mutual funds is the cheapest option.

Q: Should I create my own index funds or use a robo-advisor like Wealthfront?

A: It depends on your personal preferences and investment goals. Creating your own index funds can give you more control over your portfolio and potentially save you money on fees. Using a robo-advisor can be a good option if you prefer a hands-off approach and want access to additional services like automatic tax-loss harvesting.

Q: What are the advantages of creating your own index funds?

A: Creating your own index funds will have lower fees, greater control over your portfolio and the ability to customize your investments to your specific needs and goals.

Q: What are the advantages of using a robo-advisor like Wealthfront?

A: Using a robo-advisor like Wealthfront includes access to professional investment management services, automated portfolio rebalancing and tax-loss harvesting to potentially reduce your tax liability.

Disclaimer:

I am not a certified financial planner and the opinions expressed in the Blog are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security or investment product. It is only intended to provide education about the financial industry. Always do your own research and invest at your own risk.